The smart second mover

A European strategy for AI

This post is co-authored with Jesús Saa-Requejo.1

The United States and China are pouring hundreds of billions of dollars into gaining a first-mover advantage in AI. The natural reflex is to join this race—to build a “sovereign” AI to compete.

This would be a costly mistake. First, it is not clear who will capture the value of AI. Investment in compute or in foundation models is a large bet on just two of many potential futures. Value may be captured instead by the hardware (NVIDIA, TSMC, ASML) layer, or, as we elaborate here, by the implementation layer.

Second, it is unlikely that Europe will succeed at catching up. There are fundamental issues: a lack of a pre-existing tech ecosystem; energy costs that are 2-3 times higher than the US; and planning processes that make building near impossible. There are also the self-imposed problems we have documented in this blog: a regulatory framework that actively discourages both learning from data and digital entrepreneurship; infrastructure that is deliberately fragmented for political reasons; and labor markets that make failure prohibitively expensive.

But Europe's weakness in building models hides a strength. Europe today is in a somewhat similar position to 19th-century America or Germany with respect to the United Kingdom.2 The continent may not have invented the new technology, but it has the raw size to do well in its application: a vast, partly unified market, a highly educated workforce, and a collection of world-leading industries in machine manufacturing, pharmaceuticals, and automotive that stand to gain a lot from AI. The question should not be how to catch up in model-building, but how to convert our immense size into a new kind of scale advantage. This is where a smart second mover strategy becomes essential.

The second mover

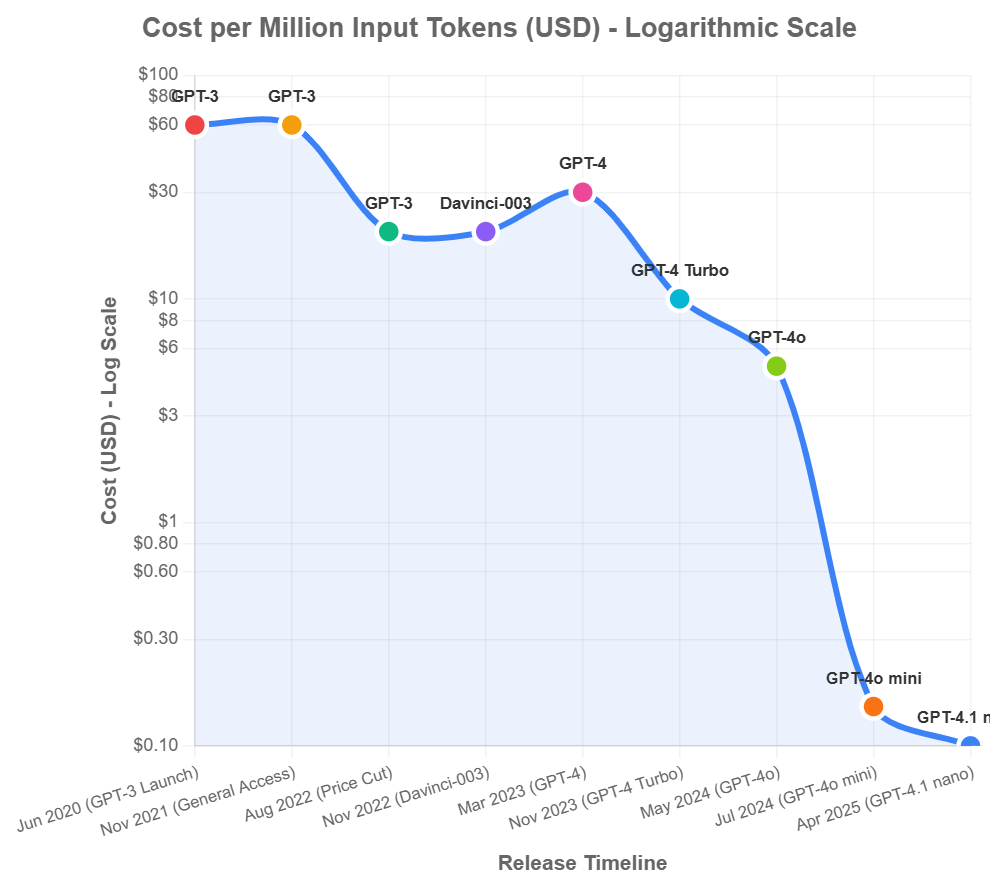

A smart-follower strategy means shifting from trying to create foundational models to becoming a sophisticated and rapid user of AI. If (artificial) intelligence becomes commoditized, as the collapsing costs per token of several competing similar manufacturers suggests, model creators won't capture economic value. Instead value may be captured by the firms and industries that integrate AI most effectively. The central challenge, then, is to avoid the fate of our telcos, which became “dumb pipes” for data used by American big-tech, or our hotel industry, which pays tribute (with fees up to 30% of the total) to a single (albeit European!) booking platform. We must prevent a future where Europe’s industries are mere commodity users of foreign AI, with all the value extracted by a few gatekeepers in Silicon Valley.

This strategy comes down to two principles: speed and competition.

First, we need to move fast, to win the race to adopt. Our primary advantage is not invention, but integration. Instead of our current instinct to regulate first, we must let our companies experiment freely and quickly. We need to clear the obstacles for our industries to embed AI into their factories, labs, and offices with minimum cost and delay.

Second, we need to do our best to maintain a competitive market for foundation models, even if it requires forcing the market open. We must use the power of our single market to ensure fierce competition among AI providers. Social media monopolies taught us a costly lesson. Without forcing platforms to be interoperable and letting users own their data, the biggest players won and achieved lock in. Imagine how different the world would have been had users owned their own data and their friends lists. You could follow friends irrespective of their platform, so that when they post something their friends will see it regardless of whether they are in Threads, Twitter, and Bluesky. No lock-in. Our rules must enforce open standards that allow European companies to switch AI providers easily, own their innovations, and keep the profits they generate.

To achieve speed and competition requires requires action in five areas.

Deregulate

Instead of preemptively regulating hypothetical harms, we must create an environment where companies can experiment and deploy AI solutions quickly. There is currently a window for changing the AI Act: at a minimum, the Article 6 and Appendix III provisions of the Act, which govern manufacturing and health care, need to be removed. Other good candidates include: the transparency, logging and conformity-assessment obligations of Article 52 which impose burdens on model deployment; the GDPR's limits on fully automated decisions on Article 22 (“The data subject shall have the right not to be subject to a decision based solely on automated processing”); and the revised Product Liability Directive’s extension of strict liability to AI-driven products. It is fine not to have model developers, and not to host data centers. But that requires compensating with a regime that relies on ex-post regulatory review rather than ex-ante approval, and include sunset clauses requiring that the regulation is renewed only in cases of demonstrated harm.

Open standards

The EU's regulatory impulse must pivot from safety to value capture. To prevent AI monopolies from extracting all economic surplus, we must use our market access as leverage. Rather than forcing technology transfer, we should mandate interoperability and prevent lock-in. Rules must require foundational models sold in Europe to provide standardized APIs, allowing companies to switch between providers without costly retraining. We must also mandate data portability, so companies can extract their fine-tuning data in standard formats, and forbid exclusive dealing arrangements. The Payment Services Directive (PSD2) offers a precedent. By forcing banks to open their APIs, Europe created a competitive fintech ecosystem without having to build new banks from scratch.

Data advantage

Instead of vague “data infrastructure,” Europe should create industry-specific data commons to give our companies a decisive competitive advantage. In manufacturing, we can scale up Germany’s Manufacturing-X initiative continent-wide, aggregating anonymized production data to create industrial AI training sets no single company could assemble. In health, we must move past the obstacles and exploit the advantage of our universal healthcare systems by pooling anonymized patient records and genomic information. (The European Health Data Space regulation, implemented in March 2025, tried to be a step in this direction but critics worry that its regulatory and administrative burden will sharply reduce its usefulness.) This would give our pharmaceutical companies unmatched training data for drug discovery.

Tax incentives for AI integration

We should aggressively subsidize AI integration. This could include large deductions for costs tied to embedding AI in production processes, accelerated depreciation for AI hardware and software, and targeted tax credits for collaborative R&D projects. Ireland's 25% R&D tax credit helped make it a tech hub; a stronger, AI-specific version could drive rapid adoption across all of European industry.

Learning

No one knows what the education system for the AI era looks like. Europe should treat its fragmentation as an asset for discovery. The EU’s role should be to facilitate and compare national experiments, running randomized controlled trials to learn what truly works and creating a framework to share best practices. By running multiple educational models in parallel, we can discover faster how to best prepare our next generation for the future.

Will this work?

Critics of this bet will raise two main concerns, one external, one internal. First, can Europe (or anyone else) capture value from AI without controlling the foundational layer? Second, can we implement such a strategy?

On the value capture hypothesis, the mobile phone ecosystem offers both a warning and a path forward. Apple and Google control the operating systems and capture enormous value. But, while telcos have indeed become just dumb pipes, European companies like Spotify and SAP have built global giants on top of these platforms. They avoided commoditization by creating their own distinct advantages. For AI, the lesson is clear: Europe’s industries must not become mere interchangeable users of foreign models. The goal is not just to use AI, but to implement it in ways that are hard to replicate. This requires developing proprietary data. It also requires building switching costs through deep integration. This is how Europe avoids the fate of its hotel industry.

Regarding implementation, we must apply to ourselves our own argument on industrial policy. The question is not if industrial policy works in general, but if the conditions are here for this proposal to work in Europe now.

Are the conditions here? The full answer would require a full post. But two hard steps are evident. Our proposal requires politicians to face reality and admit that the race to get to the frontier is lost. Even harder is managing the clash of our approach with Europe’s regulatory culture. The precautionary principle, requiring that potential risks be regulated before they materialize, is the enemy of innovation. It impedes the messy work of trial and error that allows new technologies to become established. Whether Europe’s politicians can transcend that remains to be seen.

In sum, Europe's choice is not whether to build a foundational AI—a costly and likely futile ambition—but how to capture the technology's value. The optimal path is a smart-follower strategy, pivoting from invention to intensive application by leveraging the continent's assets: our world-class industries, skilled workforce, and huge unified market (yes, making the single market work is a necessary conidition for all of this). This approach requires political courage to abandon prestige-driven “sovereignty” rhetoric for the tangible benefits of adoption. It demands regulatory flexibility to enable the rapid experimentation essential for integrating AI, and unprecedented industrial coordination to build collective data advantages. By focusing on deep AI integration within its leading automotive, pharmaceutical, and manufacturing sectors, Europe can lead the economic transformation where it matters most, securing its prosperity and avoiding a future where its industries become mere commodity users of foreign technology.

Jesus Saa-Requejo is chairman of Fondation L'Ontano and Board member at Vega Asset Management Holdings Ltd.

See the interesting discussion on size and scale focused on China versus the US in this China Talk interview with Rush Doshi.

One of the main points to take away in my opinion is the importance of regulating open standards. This is perhaps one of the most important and underrated roles of government. The establishment and enforcement of standards on weight were important in their time to establish trust between merchant and buyers. In that same way, establishing standards for AI APIs would be very important in taking away risk from developing tools that integrate these models as well as fomenting competition and innovation.

It’s striking that this article highlights the importance of tech diffusion, yet criticizes an online travel platform that has significantly accelerated the digital transformation of small European hotels. In reality, partnering with platforms has enabled independent accommodations to adopt online distribution tools, expand their reach, and improve performance – as this study shows: https://www.emerald.com/insight/content/doi/10.1108/tr-03-2020-0101/full/html.

In fact, it’s likely no coincidence that the accommodation sector is the only one in Europe to see productivity gains within firms (https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op268~73e6860c62.en.pdf). With nearly every hotel now marketing and selling online – often through platforms – the sector has become more efficient and better able to utilize its capacity by connecting to international demand.