The two Europes

Europe’s security shock is deepening its economic divide

(I coauthored this post with Olivier Kooi who is a postdoc at the LSE.)

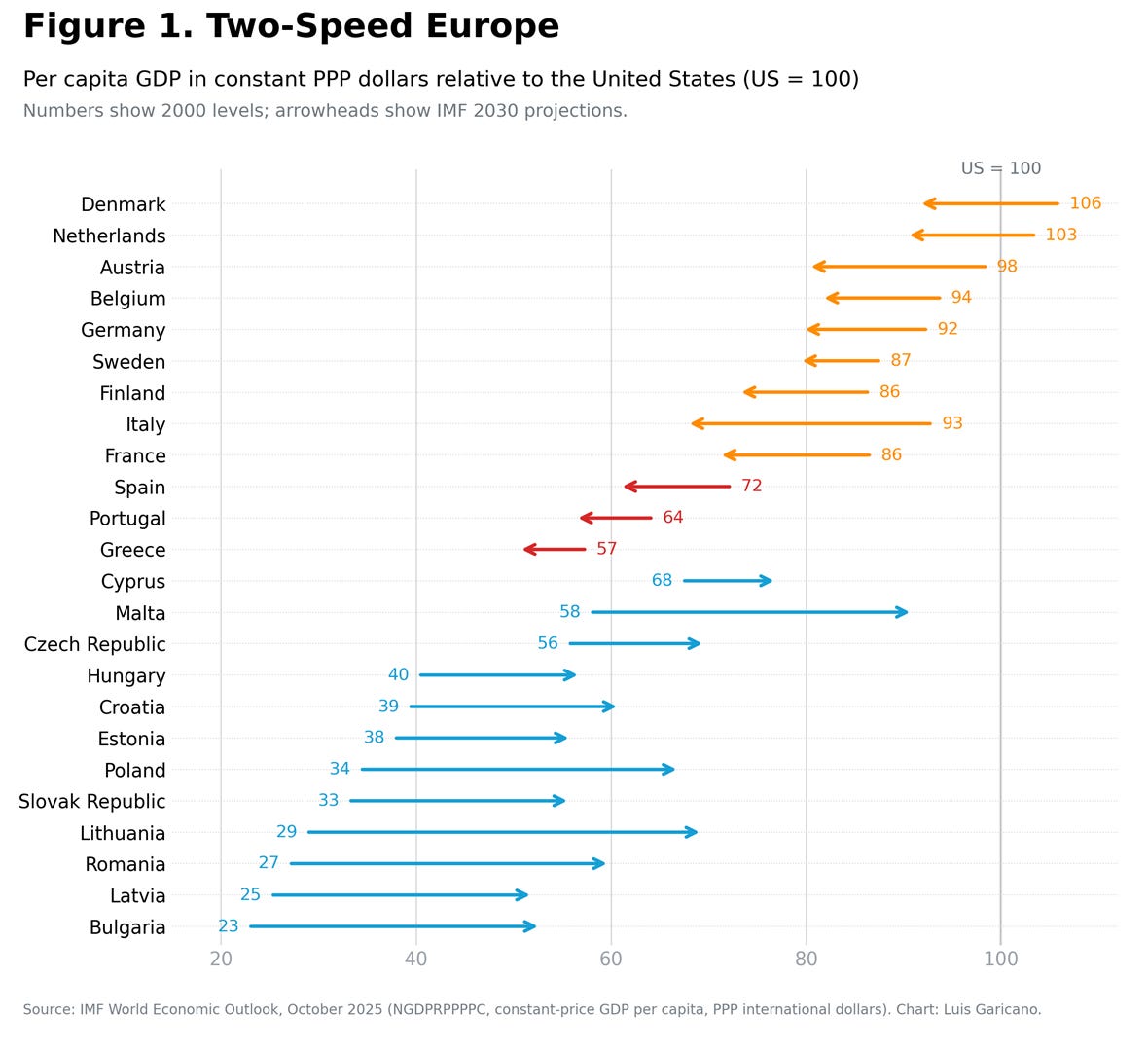

While we have spent a decade complaining about Europe’s stagnation, Eastern Europe has experienced convergence. Poland entered the millennium at 34% of US per capita GDP; by 2030, the IMF projects it will reach 67%. Romania rises from 27% to 60%; Lithuania, from 29% to 69%; Bulgaria, from 23% to 53%. These countries’ citizens are still significantly poorer than Americans, but they have closed a large part of the gap with the frontier. Across Central and Eastern Europe, the EU has functioned as a convergence machine.

Meanwhile, at the other end of the continent, the picture is almost the mirror image. Portugal slipped from 64% to 57%. Spain fell from 72% to 61%. The richer laggards are more striking: France dropped from 86% of the US level to 71%, and Italy fell from 93% to 68%.

This split explains why the recent debate about whether Europe is “really” stagnating has been so unsatisfying. Gabriel Zucman and others such as Krugman and Saez point to the convergence numbers and argue that European growth has been underestimated. Philippe Aghion and others insist that Europe has fallen badly behind on productivity and innovation. Both are right, but about different countries. The Saez-Zucman story is true for the Eastern half of the chart: rapid catch-up from a low base, driven by capital deepening and institutional convergence after EU accession. The Aghion story is true for the Western and southern half: rich countries that have not kept pace with the US frontier in the technologies that now drive growth. The EU is two economies that move in opposite directions. This fracture already existed before Russia’s full-scale invasion of Ukraine in February 2022.

The hope in Europe after the Draghi report was that the Russian threat to the east would supply the urgency the reform agendas in the “stuck” part of Europe lack.

Sadly, the correlation created by the crisis is the wrong one. The Russian shock is mobilising the countries where the Draghi problem is not most severe, and leaving untouched the countries where it is most severe. War is reforming Europe’s frontier, not Europe’s rear.

Mancur Olson saw this coming. In The Rise and Decline of Nations (1982), he argued that long-stable societies accumulate “distributional coalitions” over time. Producer associations, trade unions, professions, public sector constituencies, regional lobbies, and business incumbents learn to maximise the rents they receive from the current institutional setup. None of them is large enough to destroy the economy on its own, but acting together they make any reform almost impossible to pass. Olson’s conclusion was that settled societies do not reform themselves voluntarily, but need something to force them to do it.

Continental Europe is Olson’s perfect example. Its democracies are old. It has gone through two decades of low growth, so there is little surplus to pay losers off, and interest groups are used to fights being zero-sum. Many of these groups are made up of old people, so there is even less reason to accept short-term pain for longer-term benefits. This is why the agenda set out in the Draghi report is so hard to deliver. Almost everyone agrees that Europe needs more innovation, more energy investment, greater defence capacity, and larger, more productive firms. Almost every reform that would deliver these things creates concentrated losers today, and is therefore blocked.

War can change the bargain. Tim Besley and Torsten Persson, in their work on state capacity, have argued that when the existence of the state itself is at stake, elites become less willing to tolerate narrow rent-seeking and more willing to fund the things that hold the state together: tax administration, courts, infrastructure, schools, a standing army.

The mechanism works where common-interest institutions are strong enough that the state can credibly commit shared resources to common purposes. Take South Korea. When Park Chung-hee took power in 1961, North Korea looked economically and militarily stronger and had Soviet and Chinese backing; Park redirected an already-functioning state apparatus toward exports, infrastructure, and education. Israel and Taiwan followed similar paths, building capable states that spend heavily on defence and make growth a priority. The opposite is the case where the underlying institutions are weak, in which case the threat converts into repression, as in Pakistan or Egypt.

Europe is a third type that does not quite fit under the existing theory. European states have high capacity, but use it to provide large consumption transfers rather than growth-promoting public goods. A security shock in such a state will raise defence spending easily. Whether it also redirects the fiscal stance toward growth depends on whether the shock is large enough to weaken pensioners and other insiders who own the claims to the consumption budget.

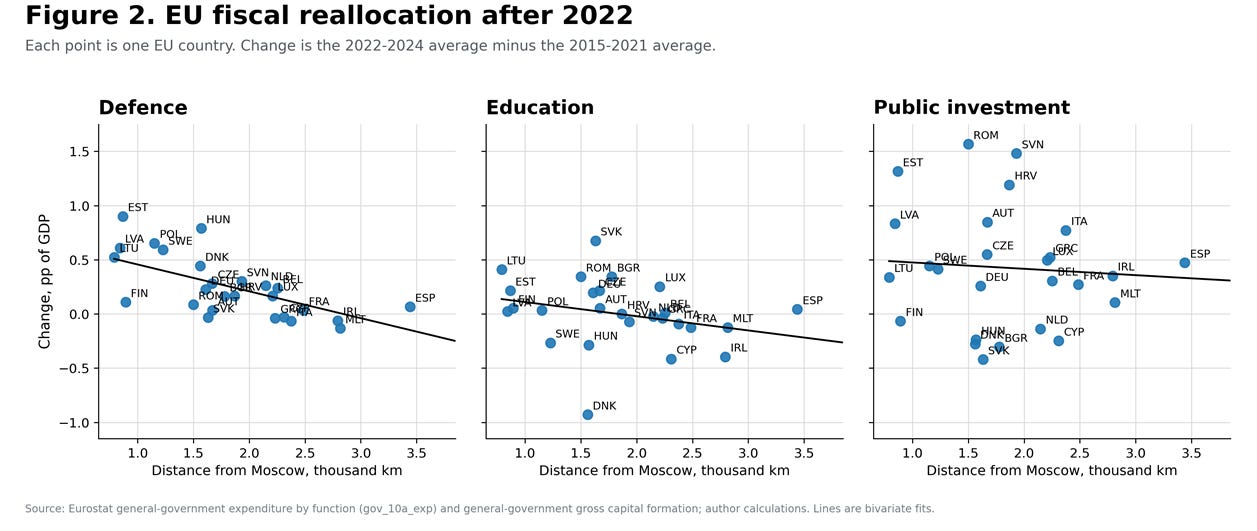

Part of Europe is mobilising

The empirical question we pose is whether after 2022 countries closer to Moscow reallocated more than their own previous path would suggest. The regressions in the appendix control for permanent country differences, common EU-wide shocks, and the separate year-by-year catch-up path of post-2004 entrants.

We find that, after controls, each 750 km (one standard deviation) closer to Moscow predicts about 0.30 percentage points of GDP larger increase in defence spending after 2022. The relationship is strong, as the left panel shows, and statistically significant (the standard error is 0.09).

The harder question is whether the war just led these countries to buy weapons or whether it also led them to invest in long-term growth. We also see increases in public investment for the countries that are close to Moscow. A state that is 750 km closer to Moscow would be expected to spend 0.39 percentage points of GDP more on government gross capital formation after 2022. Again the effect is statistically significant (standard error is 0.12). Finally, the evidence suggests that education spending also was less reduced in countries closer to Russia, by about 0.18 percentage points of GDP per standard deviation of proximity. The estimate is less precise than the defence result, but the gradient is in the right direction.

The combined bundle of defence, education, and investment moves by roughly 0.9 percentage points of GDP per standard deviation of proximity and is again significant. At minimum, frontier governments appear to be reallocating fiscal effort in a way that is broader than defence alone. Whether this becomes durable state-capacity building is too early to say.

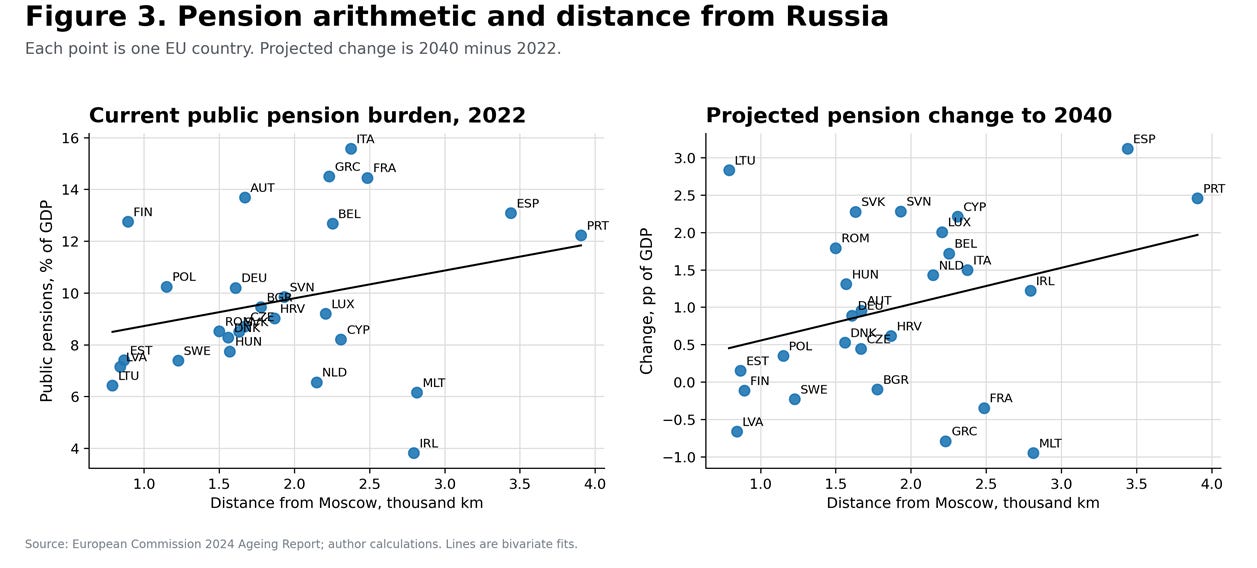

Fiscal mobilisation is not only about adding new spending. It is also about whether existing claims on the budget crowd out future-oriented investment. In Europe, the most important of these claims is pensions. Pension spending moves slowly, and we see no post-2022 effect in the data. What the figure below shows is descriptive, not causal: countries far from Moscow already devote more of national output to pensions than countries close to it, and the gap is projected to widen.

According to our calculations from the European Commission’s 2024 Ageing Report, each additional 1,000 km from Moscow correlates with about 1.07 percentage points of GDP higher pension spending in 2022, and about 0.49 percentage points more projected growth by 2040 (Pearson correlations 0.28 and 0.32).

The evidence suggests that, while war may reform Europe’s frontier, it is much less clear that it can reform Europe’s rear. For the Draghi agenda, that is the central problem.

Fear of Putin will not do Draghi’s work

The evidence suggests that the security shock is creating political room for reform mainly where the competitiveness problem is least severe. Poland, the Baltics, Finland, and Sweden are either closer to the frontier or growing faster. The shock is not creating room in the countries where the reforms in the Draghi agenda are most needed. In Italy, Spain, and France, low productivity growth, ageing fiscal commitments, and protected incumbents are the heart of the problem, and the war is, for the median voter, still a foreign-policy event.

Creating a growth coalition strong enough to take on pensioners and other insiders is something few European democracies have managed to do. Maybe Macron’s first term before the Gilets Jaunes came closest. Most likely a fiscal crisis, or a larger external shock will be needed to create enough reform pressure.

Appendix: Data and regressions

References

Besley, Timothy, and Torsten Persson, 2008, “Wars and State Capacity,” Journal of the European Economic Association 6(2-3): 522-530.

Besley, Timothy, and Torsten Persson, 2009, “The Origins of State Capacity: Property Rights, Taxation, and Politics,” American Economic Review 99(4): 1218-1244.

Draghi, Mario, 2024, The Future of European Competitiveness, European Commission.

European Commission, 2024, The 2024 Ageing Report: Economic and Budgetary Projections for the EU Member States (2022-2070).

Olson, Mancur, 1982, The Rise and Decline of Nations: Economic Growth, Stagflation, and Social Rigidities, New Haven: Yale University Press.

| A guest post by

|

Extremely insightful, thank you, Luis. One comment: (1) your Figure 1 should be reflected in sovereign bond yields (apples-to-apples, i.e., yields on the euro-denominated bonds traded on luxse.com for the non-Eurozone countries). (2) In theory, these yields should create powerful incentives to "do something" or "stop doing something". (3) But the ECB distorts these yields by its yield support program—Cochrane, John H., Luis Garicano, and Klaus Masuch. Crisis Cycle: Challenges, Evolution, and Future of the Euro. Princeton, NJ: Princeton University Press, 2025. (4) So they do not reflect your Figure 1, and, consequently, (5) do not provide correct incentives, which, in a nutshell, means that (6) Draghi's "whatever it takes" is a contradiction to Draghi's Report.

Mark blyth has been talking about this effect for a long time

https://youtu.be/nwK0jeJ8wxg?si=_lIiz-vxB992uDFS&t=18