Nineteen thoughts on AI and Europe

Protectionism and industrial policy won't fix our problems

After the events of last weekend, here are some thoughts on where Europe is with AI. This post is coauthored with my colleague Simon Grimm. You can find his Substack here.

The reporting so far seems to indicate that foreign citizens were banned from using Anthropic’s model Fable because the Trump administration needed a way to shut down access to the model for everyone – including American citizens – and export controls were the easiest way to do so. As American model regulations become more sophisticated, we should expect more narrowly targeted restrictions.

American control over models is no greater than American control over consumer and enterprise software. That arrangement has not worked so badly for Europe: Google earned a lot of money over the last twenty years, but European consumers and business enjoyed Maps, Drive, Gmail, YouTube, and Search. Artificial intelligence may be quantitatively much more important to the economy, but qualitatively the dependence is no different.

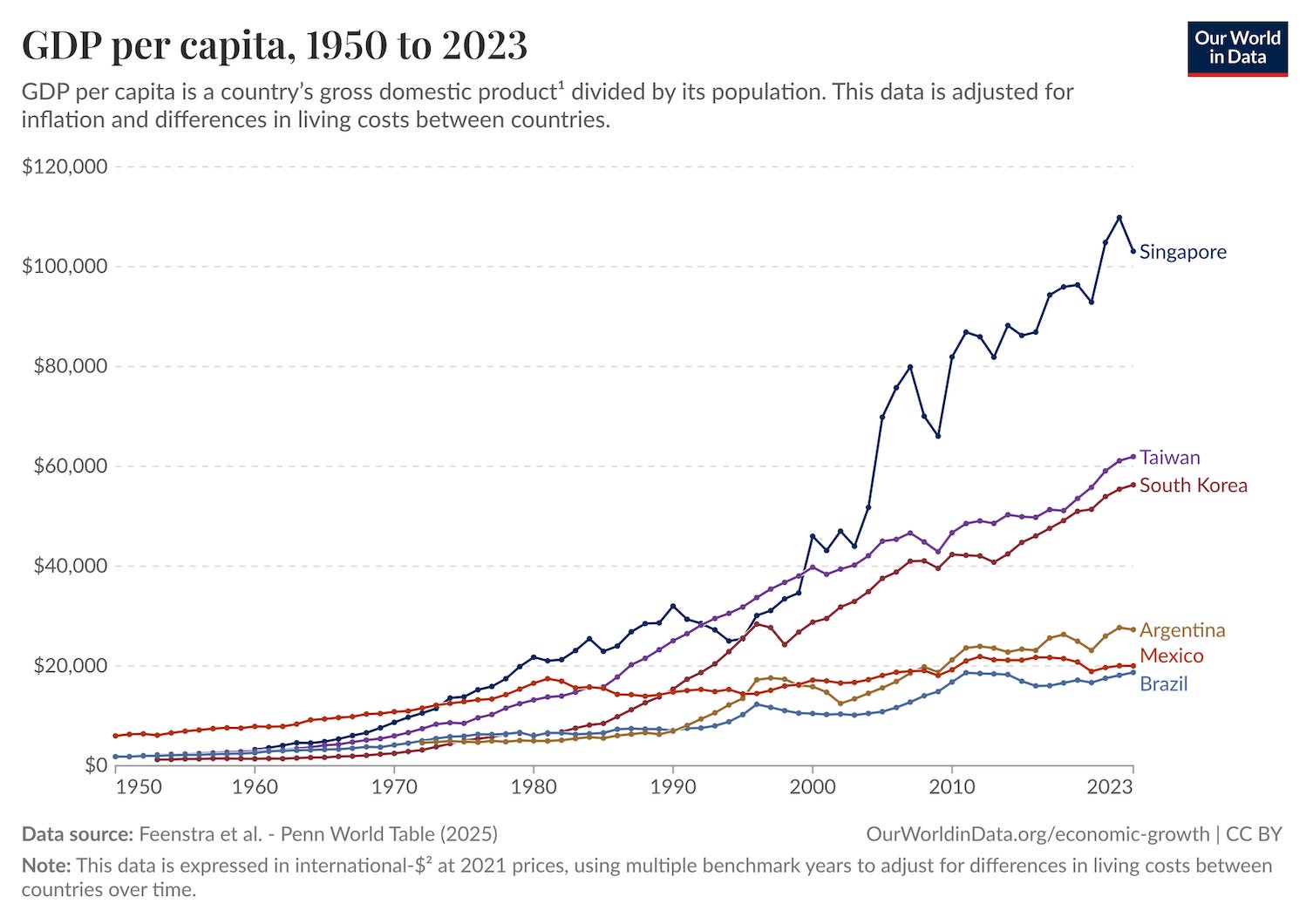

Economic convergence across history has always depended on the importation and adoption of foreign technology, not its rejection. Mexico, Argentina, and Brazil lost much of the twentieth century pursuing import substitution; Singapore, Taiwan, and South Korea have become rich by integrating themselves into global manufacturing. Even the Chinese have gritted their teeth for decades and accepted dependence on the Americans.

Dependence on American technology does not imply permanent vassalage. It seems unlikely that AI will be the only technology, or Anthropic the only company. Superhuman intelligence may make progress in plasma physics, but that will create a need for companies that build fusion reactors. Those could be German as much as they could be American.

Becoming major users of American models makes restrictions less likely because of the cost to American companies of losing European customers. Nvidia is lobbying the Trump administration to allow it to sell chips to China because of its importance as a market.

Champions of a European AI model should ask themselves if a European effort would be more effective than Meta, which this year will spend more on chips ($125 billion) than Germany spends on defense ($114 billion) and offer salaries of over $100 million to attract the best researchers, and is still failing to catch up. Elon Musk tried and failed to build a good AI model.

European governments tried to build their own Google in 2005, a Franco-German alternative called Quaero. After Franco-German disagreements, the Germans spun off Theseus. Both Quaero and Theseus were discontinued by 2013.

Fable teaches us something general about the ‘intelligence commoditization’ thesis and the ability of worse models (whether Chinese or European) to substitute for the frontier ones. Having experienced a better model, Opus 4.8 is painful to use even on tasks where it previously felt helpful.

New models can do things that old models could not do: no amount of GPT-4 prompts could solve an Erdos problem. But the preference for better models is also because returns in life are non-linear: competition between firms, applications for jobs, financial trading, and legal work share the characteristic that a tiny increase in performance can deliver enormous increases in payoffs.

In a world of highly skewed returns to capabilities, the second mover earns nothing. The revenue that Mistral reported earlier this year is less than one percent of Anthropic’s today. Any European sovereign AI effort would have to invest billions to catch up without making any money along the way.

The response to the revenue problem should not be the Buy European Tech Act, if ‘Buy European’ means buying worse models, baking in security vulnerabilities and less useful responses. (Simon has written a piece about this here.)

The above is all true if we are in a world of increasing returns to model capabilities, where companies with better models can use them internally – and the revenue they earn from them – to pull away from weaker labs. For now, this seems true: the gap between Google DeepMind on the one hand and Anthropic and OpenAI on the other has increased over the last year. In the increasing returns world, it is enormously hard for any company, whether European, American, or Chinese, to catch up with the current leaders.

This world of increasing returns is not guaranteed. Many smart people don’t believe in it: Google is selling millions of chips to Anthropic rather than giving them to DeepMind, because Anthropic’s willingness to pay for the chips — their belief in near-term progress — is currently greater than Google’s. If progress did slow down, other providers, including European ones, would be able to catch up.

We interviewed a number of European data centers over the last two months; all said that European data centers would not be built at scale without subsidies. Part of this is due to Europe’s high power prices and population density. In the areas where these problems are less pressing – Scandinavia and Iberia – smaller data centers are being built by commercial providers.

A reason why American companies don’t want to build their biggest data centers in Europe is political risk. The companies worry that the European Union will change its rules on copyright, fine them, and come up with extractive taxes once the investments are committed.

It may seem implausible for a democracy to commit economic self-harm on that scale. But, through the energy transition, Europe has signaled that governments will tolerate destroying industries as important as the German car and chemical industries. It is not clear how you rebuild this trust.

If it does come down to a transatlantic stand-off for model access, the upside of combining forces in the European Union may be lower than the downside of increased coordination costs. There are many members of the EU with conflicted interests who might yield to pressure: Eastern Europe needs the American military presence in Europe to deter Russia. Having countries like these involved in decisions may diminish total European leverage.

It would be helpful for national leaders in Europe to think about AI from the perspective of their national interest. The member states are the ones that control the factors that matter: labor markets, taxes, permitting, and energy. The Netherlands could choose to loosen the planning laws that are slowing the expansion of ASML; Germany could lower its electricity costs enormously with a nuclear restart. They have far more control over their individual destinies than does the European Commission.

| A guest post by

|

Hey Pieter! It's been a long time since we've last spoken (high-school CGU times...), but I recently stumbled upon your substack because of the interest/worry in rapid AI development that we apparently share.

I'd like to refer you to this article; https://europe2031.ai/ (there is a TLDR here: https://europe2031.ai/summary/) which was published this week. It relates to some of the points you list in the post, and I find it to be quite a convincing case for how the future might turn out if we don't take drastic action.

Simplistic analysis. Every point is valid, but it omits the most important one: if you don’t have vibrant internet companies, you don’t have the talent base needed to build internet giants. If you don’t have internet giants, you don’t have the talent base needed to build AI giants. So every time Europe—or anyone else, for that matter—delays the development of giants in the current leading technology, it also dramatically reduces its chances of playing a meaningful role in the next technological breakthrough.