Do we need banks?

The Digital Euro’s Bizarre Design

Imagine Apple launching an iPhone designed to be worse than the previous model. That's what the European Central Bank is doing with the digital euro project.

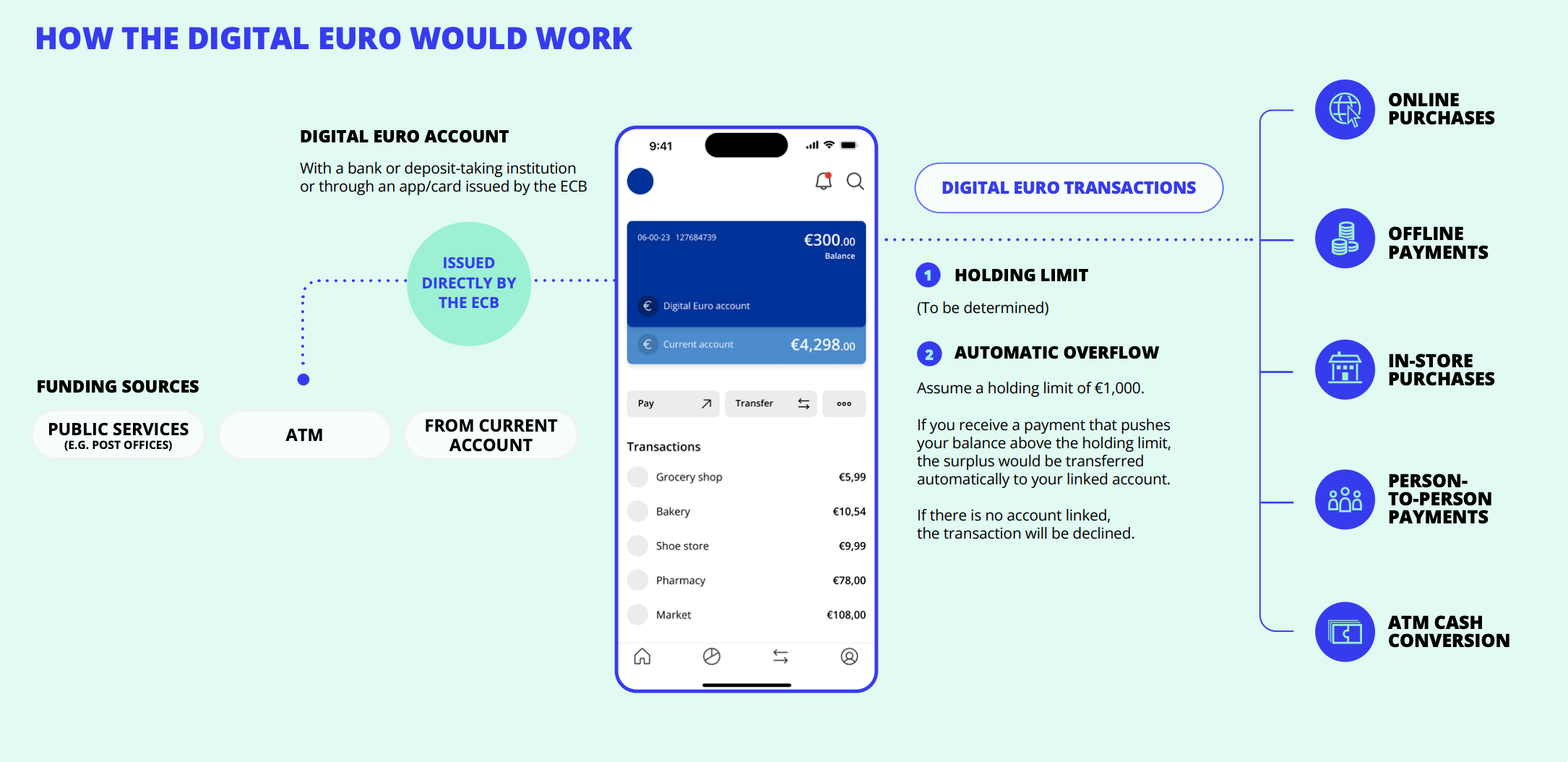

The goal of the digital euro is to give everyone a wallet held at the central bank. European citizens would be able to store money and make payments directly from an account at the European Central Bank, instead of using private banks.

The introduction of Central Bank Digital Currency (CBDC) is a response to private digital currencies like Bitcoin. This is how monetary innovation has happened historically: private monies fill gaps in the official monetary system — for instance, providing small denominations when public currency don’t — but are typically short-lived as public money systems adopt their features.1

CBDC aims to incorporate the elements that make private digital currencies attractive — from their programmability through smart contracts to instant, low-cost cross-border payments. The goal is to make payments easier and cheaper, improving the value proposition of public money. At the very least, merchants and consumers would avoid paying the fees charged by oligopolistic card issuers (Visa and Mastercard).

Peculiar Design Choices

This makes the ECB’s design choices all the more surprising. The ECB limits the digital euro's usefulness by imposing:

No interest payments on holdings

Strict limits on the amount of money individuals can hold in their wallet

Mandatory linkage to bank accounts for amounts over the holding limit, with excess amounts automatically transferred to linked bank accounts or transactions declined

It's like designing a fantastic new car but limiting it to 30 mph to avoid competing with existing taxis. Who would buy such a car?

In the ECB’s view this is necessary to preserve financial stability:

“To preserve the economic function of commercial banks, individual digital euro holdings would be limited. Merchants would be able to receive and process digital euros, but would not be able to hold them at all ‒ protecting the corporate deposit base of the banking system.”

This seems peculiar. Historically, central banks have accepted private deposits — in 1900, half of Spain's deposits were held at its central bank, and the Bank of England allowed individual accounts.2 Banks hold enormous reserves (€3 trillion) in their ECB accounts — effectively money in an interest bearing ECB account. Why should citizens be different?

The risk of destabilization the ECB is worried about stems from the transition. Banks have used deposits to provide long-term loans. If the digital wallet had no limit, offering a safe and fast means of payment, deposits might flood out of banks, creating a mismatch with their illiquid long-term loans.

Disintermediation of Banking

But beyond the transition costs, is the banking system worth protecting? The traditional justification is that banks serve a unique and vital economic function through “maturity transformation” — converting our liquid, short-term deposits into long-term loans like mortgages. This narrative is at odds with reality:

Non-bank lenders handle 55% of U.S. mortgages

Private credit funds manage $2 trillion globally

Payment processing has been transformed into software by companies like Stripe

Specialized private equity funds are disrupting traditional corporate lending

Almost every core banking function is now done more efficiently by specialists. But banks retain one distinctive feature. While specialized firms have taken over most banking functions, they haven't inherited banking's fundamental vulnerability: the susceptibility to runs. This critical flaw, rather than any special economic function, has become the defining characteristic of modern banking, demanding ever-larger state guarantees to maintain stability.

Banks are mainly financed with debt (including deposits), which accounts for about 90% of bank assets. Banks consider onerous the regulatory (Basel III) requirement that their leverage ratio (the share of capital out of total exposure) be 3%. Hence, even a small drop in asset prices turns banks insolvent, forcing them to sell holdings at fire-sale prices, creating a doom loop of falling values and mounting withdrawals.3

The Northern Rock's 2008 collapse demonstrated a “traditional” bank run, with customers queuing at the bank doors. But modern runs happen at the speed of social media, as seen with Silicon Valley Bank's WhatsApp-coordinated exodus. As runs have evolved, so has the state's solution, deposit insurance. It has become an elaborate fiction: officially it protects small depositors while maintaining market discipline — in practice it expands to cover all deposits during crises.

Recent examples demonstrate this pattern:

All deposits in Northern Rock were guaranteed by the United Kingdom in 2007

The Irish state guaranteed the entirety of the deposits of the Irish financial system in 2008 and subsequently went bust as a result. Germany immediately imitated it

In March 2023, the US Treasury invoked a “systemic risk exception” allowing Signature Bank and Silicon Valley Bank's uninsured depositors to receive full protection beyond the insured $250,000 limit

With subsidized funding, banks take large risks. One current example is US banks real estate portfolios. Banks hold about $2.7 trillion in commercial real estate loans. These loans, often guaranteed by empty (post Zoom) office buildings, account for about 25% of their business, and are worth a lot less than what appears on their books. Given the tiny sliver of equity available, many banks are underwater. Erica Jian and her coauthors show that with a 10% CRE default rate —modest by historical examples— the median US bank has negative equity. The only reason they avoid a run is deposit insurance.

Density of the equity to asset ratio, valuing all non-equity bank liabilities at its face value as of 2024. Q1 and given CRE distress scenario assuming 10% default rate on commercial loans at each bank and a 30% loss given default. Source: Jiang, Erica Xuewei, Matvos, Gregor, Piskorski, Tomasz and Seru, Amit, Monetary Tightening, Commercial Real Estate Distress, and US Bank Fragility (April 4, 2023).

The scale of the intervention, which has grown with each crisis, will certainly grow in the next. The combined balance sheets of recent US bank failures (Silicon Valley Bank, Signature Bank, and First Republic Bank) surpass the combined assets of the 25 banks that collapsed in the 2008 financial crisis. The Swiss central bank provided almost CHF168 billion in assistance to Credit Suisse.

Banks have effectively established a model where they:

Collect government-guaranteed deposits

Make risky investments with those deposits

Keep profits during good times

Receive taxpayer bailouts when things go wrong

Could We Do Without Banks?

Banks are losing utility, and they have become unwieldy and risky. Could we do without them? There are two main objections.

First, banks function as the state's financial monitoring infrastructure, aiding in tax enforcement and anti-money laundering efforts. In 2022, U.S. financial institutions filed over 3.6 million Suspicious Activity Reports (SARs). On paper, a Central Bank Digital Currency could solve this problem at lower cost. But in Europe’s case, the ECB has emphasized privacy — not surveillance — as a key feature of the digital euro. The ECB aims to make the digital euro as anonymous as using cash. This creates a paradox: if it offers stronger privacy protections than bank accounts, it could weaken anti-money laundering efforts. Ideally, the ECB would treat large transactions in the digital wallet like we treat large cash payments today — governed by monitoring requirements — while keeping small payments private.

Second, banks perform maturity transformation — taking money from depositors who can withdraw anytime and give out long-term loans like mortgages. But do we really need banks to do this anymore? Many other financial institutions and modern services can connect people who want to save money with those who need to borrow without taking on as much financial risk as banks do. As the graph below shows, the entire U.S. shadow banking system operates with less leverage than banks — on average half as much.

The Digital Euro dilemma

How would the deposits at the ECB be turned into loans? The ECB could be obliged to buy market rate European public debt with the proceeds from issuing the digital euro, while lifting restrictions on remuneration and amounts of digital euros held by private households or non-bank firms. This would give us a world with (much) greater stability and similar liquidity, while keeping interest rate and default risks on the CB balance sheet minimal.

Instead, the ECB is trying to thread an impossible needle: make the restrictions tough enough that it protects banks, while keeping the digital euro attractive enough to encourage adoption. With the current design, the adoption will probably be minimal or non-existent. All this is to protect the (subsidized) profits of the largely inefficient traditional banking system.

The ECB has two choices. First, it can design the best digital euro possible to encourage adoption. In this case, most of the restrictions on its use will have to go, since they undermine the wallet’s functionality, and people will rightly not understand why banks earn interest on their digital euros (called “reserves”), while citizens do not.

Second, the ECB can follow the Federal Reserve and the Bank of England’s wait-and-see approach. Bank of England Governor Andrew Bailey asks:

“The final step is to ask whether other things really are equal, or whether there are reasons why in the retail space, digital payments need to be done in a newly created Central Bank Digital Currency? A priori, I think the answer to this is that commercial bank money — i.e. banks — is the best home for such innovation.”

Digital currencies offer a chance to reimagine our financial system, but Bailey asks us to consider whether central banks are the right institutions to lead this innovation. Concentrating deposits at the ECB could create new risks even as it solves old ones. The ECB's current approach fails on both fronts: it creates a digital currency too restricted to be useful while simultaneously preserving all the weaknesses of our existing financial system. This gives us the worst of both worlds — neither innovation nor stability.

Thanks to Amit Seru, for comments on an earlier draft.

References

Brzezinski, Adam and Palma, Nuno Pedro G. and Velde, Francois R., Understanding Money Using Historical Evidence (April 5, 2024). FRB of Chicago Working Paper No. 2024-10.

Paul De Grauwe and Yuemei Ji . “The extraordinary generosity of central banks towards banks: Some reflections on its origin”. VoxEU 15 May 2023.

Goldstein, Itay, and Ady Pauzner. "Demand–deposit contracts and the probability of bank runs." the Journal of Finance 60, no. 3 (2005): 1293-1327.

Jiang, Erica Xuewei, Gregor Matvos, Tomasz Piskorski, and Amit Seru. "Banking without deposits: Evidence from shadow bank call reports." NBER working paper w26903 (2020).

Jiang, Erica Xuewei, Gregor Matvos, Tomasz Piskorski, and Amit Seru. “Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?” Journal of Financial Economics, September 2024. Vol. 159.

Brzezinski et al (2024).

Brzezinski et al (2024).

Goldstein and Pauzner (2005).

Thank you for your thoughtful articule! I would bring some points into the potential risks associated with central bank-controlled deposit systems and alternatives to addressing current banking inefficiencies. Let me briefly engage with your arguments:

1. Public Debt and Reckless Fiscal Policies:

There risk of moral hazard. If the ECB (or any central bank) is forced to absorb public debt, countries might indeed feel less constrained in pursuing fiscal discipline. This could amplify political pressures on the central bank, jeopardizing its independence. While current banking regulations already expose us to some of this risk, centralizing deposits could indeed magnify the issue.

2.Liquidity and Concentration Risks:

The point about systemic vulnerabilities in the event of a public debt crisis is crucial. Concentration at the central bank during a panic might intensify inflationary pressures or cause liquidity crunches. These cascading effects could undermine economic stability rather than bolster it.

3.Market Liquidity for Public Debt:

The lack of liquidity to support adequate market operations by the ECB in such scenarios is a sobering thought. Without a functioning market to absorb public debt at reasonable prices, the fallout could be severe, affecting bond markets and broader financial stability.

Proposal of a Dual Banking System

I would propose a two-tier banking solution:

1) Custodian Banks: These could focus on payment systems and short-term money market investments, resembling a safer intermediary role akin to brokers today.

2)Long-term Investment Institutions: Encouraging individuals to consider higher-yield, long-term investments while promoting financial education is a proactive approach. This could reduce reliance on traditional banks and foster a more informed and resilient population.

Final Thought

While centralizing deposits at the ECB may address some legacy issues of private banks, this could introduce new risks and moral hazards. A dual banking system, offers a hybrid solution that might strike a balance between stability, efficiency, and market discipline.

Thanks again for your detailed critique of the current banking system! Your insights add depth to the ongoing conversation about the future of banking!

Thank you very much, Luis.

It is a wonderful post to give some thought to the nature of money and the strange business model of commercial banking.

Years ago I was a director of the Caja de Ahorros de Gipuzkoa - San Sebastián and I understood the "feet of clay" of the business perfectly summarized by its President: "If Gipuzkoa goes well, Kutxa will go well" which is nothing more than confirming that if the assets (of Gipuzkoa) do not deteriorate, the balance sheet of the bank will be healthy and so will its business. In line with your reflections, I think that commercial banking does an additional job that you do not mention that is "risk redistribution". Let me explain: if there were only the ECB, all the risk (at least banking) would be concentrated there. With multiple banks (and if they are not systemic, even better), the risks are redistributed and the system does not collapse. If the ECB collapses, the whole system collapses. It is true that the ECB can print whatever it wants. If it collapses, we would go to a hyperinflation like the German one of the last century. Good post to keep thinking.